The Iran War has tightened global gas markets, but Russia no longer has the flexibility, routes, or market power to turn turmoil into strategic gain.

When the Iran War disrupted shipping through the Strait of Hormuz and tightened global gas balances, a familiar assumption quickly resurfaced: Russia, possessing the largest proven natural gas reserves in the world, would inevitably emerge as one of the principal beneficiaries. In a tighter market, the logic ran, any large gas producer with spare molecules should gain leverage. But the real question is not whether Russia still has gas—it does. The question is whether it still has the export system that once turned gas abundance into power.

Spot prices skyrocketed on European and Asian markets. Buyers rushed to find alternative suppliers. Russia’s annual natural gas production of approximately 663 billion cubic meters (bcm)—down roughly 7 percent from its prewar peak—made it an obvious candidate, seemingly well placed to benefit from any disruption to Qatari supply. Yet this intuition confuses resource abundance with export capability. Russia still has the molecules. What it no longer has is the same freedom to move them quickly, profitably, and at scale.

That is the core of the Russian gas story after four years of war. The sector did not collapse. It adapted under stress—but by sacrificing optionality, flexibility, profitability, and much of the geopolitical leverage it once derived from scale and market centrality. Russia remains a Petrostate, but a more constrained, more stressed, and far less influential one.

Russia maintained its production base. What it lost was the architecture needed to monetize that production on attractive terms: premium markets, redundant routes, commercially efficient liquified natural gas (LNG) logistics, and a buyer landscape that once feared losing Russian gas more than Russia feared losing buyers. The crisis in the Strait of Hormuzmade this structural trap externally visible. It did not create the trap; it exposed it. The trap was built before the first Iranian strike, and unless something radically changes the calculus, it will remain after the last one, too.

The contrast with oil is instructive. The transport share in the final delivered cost is far higher for gas than for oil, when pipelines, liquefaction plants, regasification terminals, and specialized LNG carriers are involved. That makes gas trade more infrastructure-intensive, more route-specific, and far harder to redirect once its original commercial geography breaks down.

Oil has shown itself to be shockingly adaptable to new strategic circumstances since 2022—Russia diversified oil exports to India, China, and Turkey with relative speed, as oil is globally traded and tanker-based. Gas does not behave that way. When a gas export system loses its core market, the problem is not simply finding another buyer. It is rebuilding an entire chain of physical and commercial infrastructure whose cost and rigidity are much higher than in oil.

That is why the last four years matter so much. They show not just that Russia lost volumes, but that it entered a different phase of gas statecraft: one defined by narrower export outlets, lower-quality monetization, and greater dependence on external political and commercial decisions. The sector has stabilized—but around a worse equilibrium.

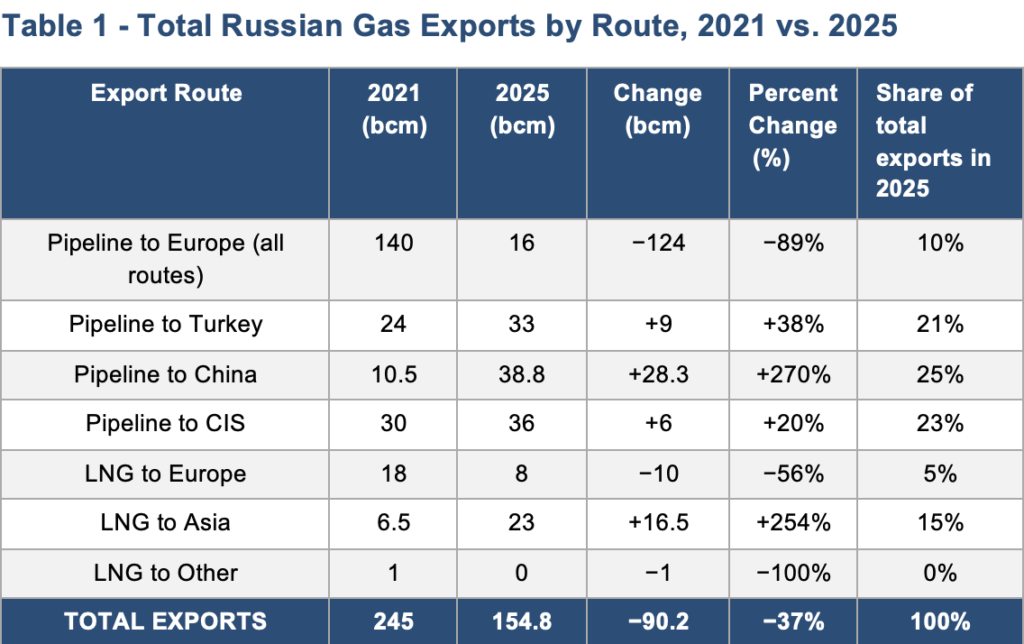

The arithmetic of this adaptation is stark: according to Gazprom and IEA data, the country lost roughly 134 bcm of gas sales to Europe (Table 1)—one of the largest demand shocks ever absorbed by a major gas-exporting system.

Lost volumes: 134 bcm (124 bcm pipeline to Europe + 10 bcm LNG to Europe)

Gained volumes: 58.8 bcm (28.3 bcm China + 9 bcm Turkey + 6 bcm CIS + 16.5 bcm Asia LNG)

Net export loss: 90.2 bcm (37 percent of 2021 total)

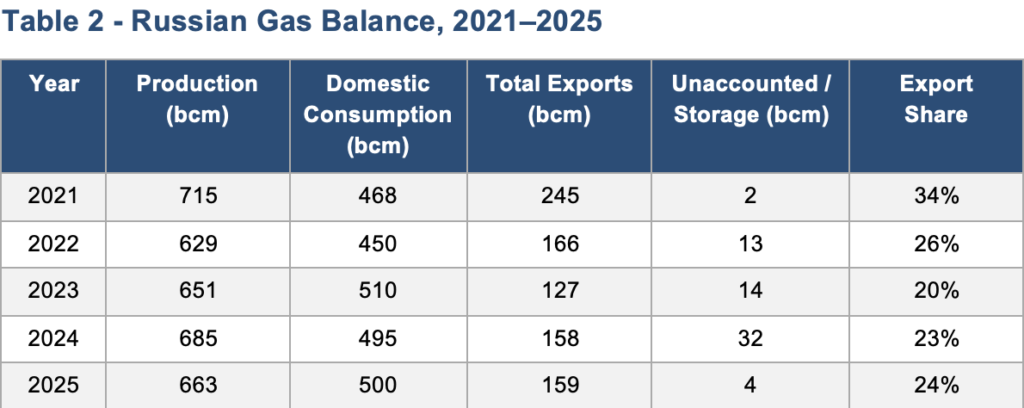

Yet total production did not implode—it fell from 715 bcm in 2021 to roughly 663 bcm in 2025, while domestic consumption rose from about 468 bcm to about 500 bcm, and new export outlets in China, Turkey, the Commonwealth of Independent States (CIS), and Asian LNG absorbed part of the remainder (Table 2). Though the share of exports in total output fell from 34 to 24 percent, the system functions, production continues, domestic demand is met, and some exports are redirected. But what was preserved in volume was sacrificed in value.

This is the central paradox of the Russian gas sector after 2022: resilience in physical terms has coexisted with degradation in strategic terms. Russia did not solve its gas crisis—it learned how to live with it.

Europe Was the Center of Gravity for Russian Gas

In 2021, Europe imported 140 bcm of pipeline gas from Russia, its most profitable market for Moscow, built over half a century of infrastructure investments. By 2025, direct deliveries to Europe outside the TurkStream corridor had effectively fallen to zero. Nord Stream 1 was sabotaged and destroyed in September 2022. Nord Stream 2, already built but short of being certified, was frozen before the invasion and never entered service. Yamal-Europe ceased operations in May of 2022. Transit through Ukraine ended in December 2024 and was not extended. As long as the war continues, there is no realistic basis for restoring that route.

What remained is one narrow corridor: around 16–17 bcm via TurkStream Line 2, reaching Serbia, Hungary, and Austria through Turkey. That route is already operating near its physical limit.

The previous model cannot be restored under anything like previous conditions. Three of Nord Stream’s four strings are physically destroyed. Political conditions allowing the functioning of Yamal-Europe no longer exist. And the Ukrainian route is not just closed; it is politically inseparable from the war itself.

Even if some bilateral flows eventually resume, the era of Russia as Europe’s central pipeline gas supplier is over. What has been lost is not just trade, but the market around which Russian gas power was built.

This matters because Europe was the market that made Russian gas strategically powerful. It combined high netbacks, long-term contracts, large creditworthy buyers, dense infrastructure, and a degree of buyer dependence that gave Moscow real leverage. Losing Europe, therefore, meant more than losing sales. It meant losing the commercial and political center of gravity of the entire sector.

The question of Russian gas returning to Europe still comes up regularly—not only among policymakers, but among industrial consumers and business groups worried about competitiveness and long-term supply costs. Limited flows may reappear. But that is very different from a restoration of the old system. A small amount of transit through Ukraine under a political deal, or limited bilateral arrangements with a few Central European states, would not recreate the architecture of the 2000s and 2010s. Russian gas could return to Europe only as a constrained, politically contingent residual flow—not as the organizing backbone of the continent’s gas balance.

What about the other markets for Russian gas? Central Asian markets partially absorbed some excess volumes. Uzbekistan became a buyer of approximately six bcm annually due to a decline in domestic production; Kazakhstan’s direct gas imports from Russia nearly tripled to about 3.8 bcm. Yet total CIS growth remained marginal relative to what Europe represented. It is a buffer, not a substitute.

Even Turkey, often presented as an alternative gateway, cannot fill the gap. The southern corridor has value, but not strategic scale. It is close to full utilization, Turkey is actively diversifying its supply mix, and onward deliveries to Europe remain modest. In practice, it has become a survival route rather than a platform for renewed influence. In 2026, it is the last route standing, not the beginning of a new export model.

China Can Help—on China’s Terms

The standard counterargument points to the notably increased eastward gas flows. Power of Siberia 1 delivered around 38.8 bcm to China in 2025—a sizable increase from 10.5 bcm in 2021. The trajectory is real. But its structural limits matter more than its headline growth.

Power of Siberia 1 is fed solely by Eastern Siberian gas fields—Chayanda and Kovykta—which were never connected to the Western Siberian production base that supplied Europe. The pipeline did not redirect a single cubic meter of gas previously destined for European markets. Instead, it developed a separate supply chain. And in 2024, it had reached its projected capacity; any further organic growth is constrained by both upstream and midstream limits.

The Far Eastern route should also be understood correctly. It is not an immediate breakthrough, but an incremental addition scheduled to begin supplying roughly 10-12 bcm a year from 2027. Useful, but not transformational.

Power of Siberia 2 is different in kind. With a projected capacity of 50 bcm from Western Siberian gas fields, it is the only pipeline project that could meaningfully reconnect Russia’s former European resource base to a major external market. Here, precision on timing matters. The draft outline of China’s 15th Five-Year Plan was submitted to the National People’s Congress on March 5, 2026; lawmakers approved it on March 12. The plan mentioned the pipeline—but only in the language of “advancing preparatory work.” That is a political signal, not a commercial commitment.

The price gap between the two sides, moreover, remains structurally unadjusted: China has pushed for terms much closer to Russian domestic rates.

China is not competing for Russian gas—it is negotiating from a position of patience, alternatives, and leverage over the gas volumes that have nowhere else to go. The eastward rerouting of gas, deepening Russia’s dependency on a single buyer at structurally degraded prices, is an adaptation, not a restoration of strategic influence.

That creates a new form of dependence. Even if Chinese demand grows and Power of Siberia 2 is eventually signed, the eastern pivot will not reproduce Europe. It may restore some monetization, but it will not restore former leverage. Asia can provide an outlet. It cannot, at least for now, provide a substitute for the geopolitical and commercial position Russia once held in Europe. China holds the stronger hand in any such scenario, and the pipeline, whose construction requires five years—and another five to reach workable volumes—cannot help Russia capitalize on the current Iran War.

At the same time, the Gulf shock may increase Beijing’s interest in Russian optionality. Power of Siberia 2 has mattered to China primarily as a form of strategic insurance rather than an urgent supply necessity. The Gulf shock increases the value of that insurance as a hedge against prolonged disruption in the Middle East. That makes Russia more useful to China—but not more autonomous. But even that scenario would not put Russia back in the driver’s seat. It would make Russia more important to China, on China’s terms.

LNG Was Supposed to Restore Flexibility for Russia

It is important to separate total Russian LNG capacity from actual output. Russia’s total nameplate LNG capacity is about 50.8 million tonnes per annum (mtpa), but the three core export projects—Yamal LNG, Sakhalin-2, and Arctic LNG 2—account for 48.8 mtpa of that total. Actual Russian LNG output in 2025 was about 32 metric tonnes (Mt), meaning the gap between nameplate and actual capacity is not theoretical—it is already visible in operations.

The gap is explained by sanctions and logistics. Arctic LNG 2, designed for around 19.8 mtpa, produced just 1.2 Mt in 2025—around six percent of design capacity. The main constraint is the shortage of Arc-7 icebreaking LNG carriers, required for year-round Northern Sea Route navigation. The project requires a dedicated fleet of 21 such vessels, but due to sanctions, Russia cannot obtain them, making shipping constraints and sanctions compliance—not liquefaction capacity alone—the most immediate bottleneck. Chinese shipyards have the technical capability to build more Arc-7 carriers, but there are no publicly confirmed contracts as of early 2026. If China deepens its role not only as LNG buyer but also as technology provider or logistical enabler, Russia may recover some functionality—but only by externalizing more control over its own gas future.

LNG was supposed to be Russia’s answer to the rigidity of pipelines. Instead, it has exposed a second layer of dependence. The problem is the lack of autonomous access to shipping, technology, finance, insurance, and commercial intermediation. Russia can still operate its inherited LNG capacity. But it is far less capable of scaling new LNG capacity under sanctions.

The commercial base for Russian LNG remains unusually fragile. In 2025, Yamal LNG still sent about 76 percent of production to European terminals, generating around €7.2 billion in revenue. That means Russia’s most commercially successful LNG project remained deeply entangled with European infrastructure even after pipeline decoupling. Europe’s gradual tightening of restrictions on Russian LNG does not just threaten volumes. It threatens the soft infrastructure of the trade: long-established offtake patterns, payment channels, transshipment services, shipping optimization, and the role of European companies in organizing commercial flows.

This is why the LNG story is more serious than it first appears. The issue is not merely that Arctic LNG 2 is delayed. The issue is that Russia’s envisioned LNG-based strategy for rebuilding flexibility has run into chokepoints that are external, specific, and hard to bypass. LNG has not become the great escape route from Russia’s post-2022 gas trap. It has become a reminder that flexibility itself requires an ecosystem.

One scenario still deserves attention. If a broader political deal between Washington and Moscow were ever to produce selective sanctions relief, some US participation in Russian gas or LNG projects could re-enter the picture. That possibility remains speculative, but it is no longer unthinkable amidst discussions around potential energy deals in the context of a wider Trump-Putin settlement track. Such a scenario would not restore the old model. It would mean something more conditional—namely, a partial recapitalization of the sector through external technology, services, financing, and commercial support. Russia could recover some functionality, especially in LNG and gas processing. But it would do so not by restoring its former autonomy, but by accepting a more dependent and politically reversible form of recovery. In that sense, the most optimistic scenarios for Russian gas still point in the same direction: more monetization, less agency.

Russia’s Gas System Survived by Turning Inward

One reason the Russian gas sector has not collapsed is that it has pushed a large share of its adjustment inward. With export markets shrinking, more gas has been absorbed domestically—through industry, power generation, and broader internal demand. This has preserved production and reduced the need for technically damaging shut-ins in West Siberian fields. But it has done so at sharply lower profitability.

Domestic absorption is therefore best understood as a stabilization mechanism, not a growth strategy. It allows the sector to function physically. It does not restore the rent that Europe once provided. Gas sold inside Russia or to low-priced neighboring markets supports industrial activity and social stability, but it does not replicate the external earnings, strategic flexibility, or geopolitical weight of lost exports.

There is, however, one important implication for the next decade. Russia can still try to remonetize part of its gas base not through larger exports of raw gas, but through deeper domestic processing: petrochemicals, fertilizers, ammonia, methanol, and power-intensive industrial production. The Iran War, which has highlighted vulnerabilities in fertilizer and maritime supply chains, only reinforces the strategic logic of such a move. That is not a quick fix. It is a constrained industrial strategy—one that would require investment, equipment, technology, and market access that remain uncertain.

Russia Has Gas—but No Export Flexibility

The contrast between the apparent beneficiaries of the Iran War is very telling. The United States can convert a tighter market into additional LNG flows because it has spare commercial flexibility, expanding capacity, and global destination optionality. Russia, by contrast, can benefit from higher prices only at the margin. It cannot meaningfully scale exports in response.

A price signal without an increase in supply is just a one-time revenue effect, not a strategic gain. Russia will receive a short-term uplift on a portion of its gas sales. But it no longer has the export architecture, market access, or strategic flexibility needed to turn external turmoil into a major expansion of gas power.

That is why Russia is unlikely to score a major strategic win from the Iran War. It may benefit at the margin through higher prices, tighter balances, and a renewed premium on supply security. But it no longer has the system that once allowed it to translate disruption elsewhere into leverage of its own.

Four years of data allow us to formulate a more concrete answer than “Russia was weakened.” Russia has maintained its core production capabilities, but it has lost optionality. Destroyed pipelines, a tanker bottleneck in LNG, and increasingly asymmetric bargaining positions are not temporary setbacks awaiting a diplomatic reset. They are structural traits of a sector that still produces gas but has far fewer advantageous ways to sell it.

Russia’s gas power was never simply about supply. It rested on infrastructure, flexibility, and the ability to make buyers feel the cost of dependence. Much of that architecture is gone. The crisis in the Strait of Hormuz did not reverse this—it only made these structural weaknesses visible to external observers.

The Russian gas sector is therefore in a tight spot, not because it is running out of gas, but because it is running out of attractive ways to monetize it. It has adapted to stress by becoming narrower, less flexible, less profitable, and more dependent on external political and commercial choices. Russia remains gas-rich—but increasingly route-poor, option-poor, and agency-poor. Postwar channels of partial recovery do exist: limited residual flows back to Europe, deeper Chinese participation in infrastructure and offtake, or greater monetization through petrochemicals and fertilizers. Each could ease pressure. None would restore the pre-2022 architecture. The sector’s likely future is not a grand rebound, but a more fragmented, conditional, and commercially degraded pattern of monetization.

That may be the most accurate description of the sector today: not collapse, not resilience, but structural downgrade. The Iran War does not reverse that. At most, it briefly illuminates it.

About the Authors: Tatiana Mitrova and Fyodor Dmitrenko

Dr. Tatiana Mitrova is a research fellow at Columbia University’s Center on Global Energy Policy and director of the New Energy Advancement Hub. She specializes in Russian, FSU, and global energy markets, including production, transportation, demand, energy policy, pricing, and market restructuring. She was the executive director of the Energy Centre of the Moscow School of Management SKOLKOVO, a graduate business school. From 2006 to 2011, she was also the head of research in the Oil and Gas Department in the Energy Research Institute of the Russian Academy of Sciences. Dr. Mitrova is a graduate of Moscow State University’s Economics Department (BSc.) and Gubkin Russian State University of Oil and Gas (PhD).

Fyodor Dmitrenko is a geopolitical analyst and researcher specializing in sustainable development, energy policy, and governance on the Eurasian continent. He is affiliated with Sciences Po Paris, where he conducts research under the supervision of Professor Tatiana Mitrova. He has contributed articles on developments in energy markets and international trade flows at Reuters News Agency’s CIS office and for emerging think tanks such as India’s TheGeostrata and the Paris section of the French-MFA-affiliated Andalus Committee, which deals with EU-global south relations. He has also engaged with leaders in the sustainable development field at the Guiyang Ecological forum as a Sciences Po delegate to the Tsinghua Global Youth Dialogue, and interviewed policy makers such as former Brazilian central bank head Gustavo Franco and former Swiss President Simonetta Sommaruga as the Sciences Po delegate to the Warwick Economic Summit.